联系方式

more本类最新英语论文

- 2017-09-13留学生lab report写作要点分..

- 2017-08-13爱思唯尔检索系统评价报告a..

- 2017-08-10financial coursework写作:..

- 2017-07-14英国coursework写作:desig..

- 2017-07-08美国coursework作业:how h..

- 2017-07-07美国留学coursework:全球化..

- 2016-11-16代写留学生课程作业coursew..

- 2015-12-07coursework写作范文:公立学..

- 2014-10-22西班牙法律学专业英语作业

- 2014-10-23留学生如何写发展中国家汽车..

more热门文章

- 2012-02-06代写coursework范文-enterp..

- 2014-10-22西班牙法律学专业英语作业

- 2015-12-07coursework写作范文:公立学..

- 2014-10-23留学生如何写发展中国家汽车..

- 2012-02-06代写coursework-关于迪斯尼..

- 2016-11-16代写留学生课程作业coursew..

- 2013-12-10economics coursework写作要..

- 2012-02-06coursework代写指导-school..

- 2012-02-07代写留学生coursework-代写..

- 2012-02-07代写留学生课程作业-代写co..

more留学论文写作指导

- 2024-03-31卡森•麦卡勒斯小说中..

- 2024-03-28美国黑人女性心理创伤思考―..

- 2024-03-27乔治·艾略特《织工马南》中..

- 2024-03-21超越凝视:论《看不见的人》..

- 2024-03-19《哈克贝利•费恩历险..

- 2024-03-13心灵救赎之旅――从凯利的三..

- 2024-02-22文学地理学视角下的《印度之..

- 2023-05-03英、汉名词短语之形容词修饰..

- 2023-02-07目的论视域下5g―the futur..

- 2022-07-04二语英语和三语日语学习者的..

Financial coursework写作:资本资产定价模型CAPM

论文作者:www.51lunwen.org论文属性:课程作业 Coursework登出时间:2017-08-10编辑:anne点击率:3053

论文字数:1636论文编号:org201708101140063181语种:英语 English地区:英国价格:$ 33

摘要:本文所要解决的问题是单因素资本资产定价模型(CAPM),投资者正考虑形成与股票投资相关的风险因素的自身收益预期。

我们测试这个课程的CAPM; 您将使用一个市场指数和至少20个公司的每周数据,这些公司应至少从两个部门。 考虑两个抽样期:(1)2008年1月 - 2010年12月和(2)2011年1月至2013年12月。 所需数据可从雅虎财经下载:

任务:

(1)确保您选择的公司和部门将获得高市值。

(2)使用整个样本期的数据,对每个选定公司进行时间序列回归,得到恒定和市场超额收益,并验证是否存在显着的β值。

(3)报告每个公司的alpha和R ^ 2的t-static。

We test the CAPM for this coursework; you will use one market index and at least 20 companies’ weekly data and these companies should be from at least two sectors. Consider two sample periods: (1) Jan 2008 - Dec 2010 and (2) Jan 2011 - Dec 2013 . The required data can be downloaded from Yahoo finance: https://uk.finance.yahoo.com/

Tasks:

(1) Make sure that your choice of companies and sectors would capture high market capitalisation.

(2) Using data for the entire sample period, run time-series regression on each of the selected companies onto a constant and market excess return and verify whether there exists a significant beta.

(3) Report the t-static for alpha and the R^2 for each company.

(4) Do a cross-sectional regression:

(5) Discuss your results and merits and demerits of CAPM analysis.

(6) Discuss whether your results are sensitive to sector characteristics.

(7) Word limit: 1500

Submission Due: 18th April 2014.

Brief notes:

1. Turnitin will be used to check the originality of all submitted work.

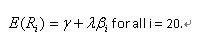

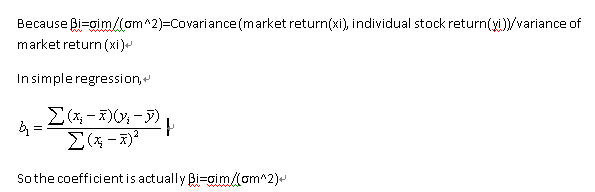

2. Why use simple regression to estimate β? Here dependent variable is stock return of individual firms (yi) and independent variable is market return (xi).

In this paper to solve the problem is the single factor capital asset pricing model (CAPM), investors are considering forming their own return expectations for risk factors associated with investing in individual stocks. They would determine the appropriate risk factors as a very important investment decision related to the stock price in the stock market formation. Therefore, the aim of this study was to investigate the theoretical and empirical validity to develop and test the capital asset pricing model.It can address and resolve the empirical shortcomings of single factor with Capital Asset Pricing Model. In order to verify the standard capital asset pricing model and the empirical validity of multi-factor model, five hypotheses were developed for testing.

Therefore, this paper introduces the error term in order to compensate for the model assumes that the rest of the state model has been caused by force factors to establish a linear regression model.Then it can make squares linear regression model simulation by time series .

共 1/1 页首页上一页1下一页尾页

英国

英国 澳大利亚

澳大利亚 美国

美国 加拿大

加拿大 新西兰

新西兰 新加坡

新加坡 香港

香港 日本

日本 韩国

韩国 法国

法国 德国

德国 爱尔兰

爱尔兰 瑞士

瑞士 荷兰

荷兰 俄罗斯

俄罗斯 西班牙

西班牙 马来西亚

马来西亚 南非

南非